ASG Analysis: Geopolitical Trends to Watch in MENA in 2020

Executive Summary

- We see the potential for growing geopolitical instability in the Middle East and North Africa this year, a continuation of last year’s trend.

- Tensions with Iran are likely to persist after reaching a new high following the U.S. killing of Iranian general Qassem Suleimani early in the new year.

- Mass protest movements that emerged last year in several MENA countries show no immediate signs of resolution and could devolve into more serious civil conflict or fuel wider regional unrest this year.

- There are bright spots, however: after a tough 2019, the Gulf economies seem poised for a modest economic recovery this year, though this will depend on global economic growth and the stabilization of oil prices.

- The potential for regional conflict and unrest, while still relatively low, further complicates the overall business and investment climate in the region. In the year ahead, it will be increasingly important for international companies operating in the region to develop and implement risk monitoring and mitigation strategies.

1. U.S.-Iran tensions likely to persist

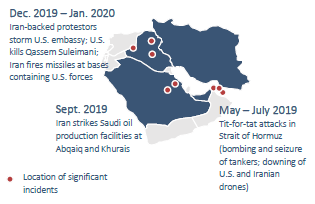

Last year witnessed the significant escalation of regional tensions with Iran. Tit-for-tat attacks over the summer (including the bombing of ships in the Strait of Hormuz and the downing of U.S. and Iranian drones) culminated in Iran’s September strike on Saudi oil production facilities at Abqaiq and Khurais, which raised fears of armed conflict in the wider Gulf region. Tensions dissipated somewhat at the end of 2019 in the absence of major new attacks but reignited in the new year following the January 3 killing of Qassim Suleimani, commander of Iran’s IRGC Quds force. This brought the United States and Iran closer to a direct military conflict than they had been in 40 years.

Last year witnessed the significant escalation of regional tensions with Iran. Tit-for-tat attacks over the summer (including the bombing of ships in the Strait of Hormuz and the downing of U.S. and Iranian drones) culminated in Iran’s September strike on Saudi oil production facilities at Abqaiq and Khurais, which raised fears of armed conflict in the wider Gulf region. Tensions dissipated somewhat at the end of 2019 in the absence of major new attacks but reignited in the new year following the January 3 killing of Qassim Suleimani, commander of Iran’s IRGC Quds force. This brought the United States and Iran closer to a direct military conflict than they had been in 40 years.

The Iranian response, which involved launching more than 20 short-range ballistic missiles at two bases in Iraq where U.S. forces were stationed, appeared to be designed to minimize casualties and give President Trump a way to avoid escalation. Trump responded by calling for additional sanctions, but he did not propose a military response against Iran, instead suggesting that the U.S. was open to making a deal. Tehran’s later admission that it accidentally shot down a Ukrainian passenger airliner and the government’s attempted cover-up triggered days of protests in Iran and demands for the resignation of senior government officials.

The months ahead will likely see continued tensions and the potential for further attacks, with the risk of a significant escalation looming in the background. Iran has already taken several steps away from compliance with the nuclear deal, and senior officials have even threatened withdrawl from the Non-Proliferation Treaty (NPT). On Februray 21, Iran holds parliamentary elections, in which hardliners are expected to do well, especially in light of the disqualification of many moderate and reformist candidates. For these reasons, negotiations toward a "new Iran deal" appear unlikely, though the possibility should not be discounted entirely.

We see three possible scenarios for the year ahead:

- Status quo (most likely): Both sides continue to denounce each other and possibly carry out low-level attacks. Although both Iran and the United States have a clear interest in avoiding war, major impediments make a new comprehensive deal unlikely in the short term. Iran has historically been willing to wait for the right moment to respond to provocations and could look to carry out an asymmetrical attack that would leave it with some plausible deniability and minimize the risk of a direct reprisal. In this scenario, the Iranian economy will likely continue to worsen, putting the Iranian regime under growing public pressure. The regime appeared to benefit from a surge in patriotism after Suleimani’s killing, a short reprieve from the mass unrest that convulsed the country in November, but this ended with the government’s downing of the Ukrainian jet and its initial denials of responsibility. In general, Iran’s economy continues to suffer under U.S. sanctions. The IMF estimated that Iran’s GDP contracted by 9.5% in 2019. The precarious economic situation and renewed calls for political reform will test Iranian leadership in coming months.

Although both Iran and the United States have a clear interest in avoiding war, major impediments make a new comprehensive deal unlikely in the short term.

- Escalation (credible alternative): One side miscalculates or deliberately provokes the other, causing an outbreak of hostilities that results in something resembling a hot war and threatens to draw in the rest of the region. While the risk of war remains low, we cannot exclude the possibility entirely. Iranian uncertainty about what the U.S. wants and what its red lines are increases the likelihood of miscalculation and inadvertent escalation. Iran could take a variety of further actions ranging from another direct attack on U.S. military personnel or the assassination of U.S. officials to cyberattacks, renewed efforts to evict U.S. forces from Iraq, attacks on U.S. allies in the region, or further steps away from the nuclear agreement, including the potential withdrawal from the NPT. Further steps away from the nuclear deal and a victory by hardliners in the upcoming elections could both increase tensions and raise the risk of escalation.

- Negotiation (outlier): The U.S. and Iran find a way to reopen negotiations. This appears relatively unlikely for now. From the U.S. perspective, the maximum pressure campaign is yielding results, and Iranian leaders are unlikely to want to be seen sitting down with Trump administration officials responsible for killing Suleimani. In the event both sides can reopen negotiations, it is most likely to result in an interim agreement in which Iran receives sanctions relief in exchange for returning to full compliance with the Joint Comprehensive Plan of Action (JCPOA), while the two sides attempt to negotiate a longer-term and potentially broader deal.

2. Unrest in multiple countries raises possibility of Arab Spring 2.0

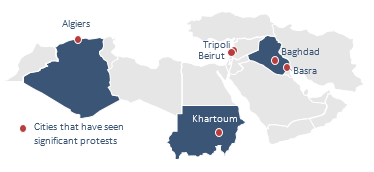

Last year saw the outbreak of mass anti-government protests in several countries in the region. In February 2019, longtime Algerian President Abdulaziz Bouteflika announced that he would seek a fifth term in office. This triggered mass protests across Algeria, which resulted in Bouteflika’s resignation in April. His departure came soon after news that the military would no longer support his leadership and was throwing its weight behind the protestors’ demands for a change in government. In Sudan, months of street protests culminated in a military-led coup d'état in April that deposed President Omar Al-Bashir after thirty years in power marked by oppression, economic mismanagement, and human rights abuses.

Last year saw the outbreak of mass anti-government protests in several countries in the region. In February 2019, longtime Algerian President Abdulaziz Bouteflika announced that he would seek a fifth term in office. This triggered mass protests across Algeria, which resulted in Bouteflika’s resignation in April. His departure came soon after news that the military would no longer support his leadership and was throwing its weight behind the protestors’ demands for a change in government. In Sudan, months of street protests culminated in a military-led coup d'état in April that deposed President Omar Al-Bashir after thirty years in power marked by oppression, economic mismanagement, and human rights abuses.

In the fall, mass protest movements gathered momentum in Lebanon and Iraq, fueled by long-brewing anger over corruption and unemployment and frustration with the political and economic status quo. In Lebanon, the protests were sparked by the announcement of several new taxes, including one on WhatsApp use, but quickly took the shape of a broader rebuke of the country’s political elites and its confessional political system, in which political power is divided among the different religious groups. In Iraq, protesters expressed similar anger with the economic situation and political elites, but also notably expressed anti-Iranian sentiments. In late October, Lebanese Prime Minister Saad Hariri and Iraqi Prime Minister Adel Abdul-Mahdi both resigned, though Abdul-Mahdi stayed on in a caretaker role until the Iraqi president appointed a consensus candidate to replace him last week.

[I]t will be important to see … whether the unrest remains limited to these countries, or, as was the case with the Arab Spring, fuels wider instability across the region, especially in the Arab Gulf states.

Unrest continues in all four countries. The military remains in control in Algeria, but its arrests of Bouteflika’s brother and other members of his inner circle have failed to pacify protestors, who demand more radical democratic change and free elections. The transitional power-sharing arrangement between the military and civilian leadership in Sudan remains fragile, and the country continues to see sporadic violence. A new government led by Prime Minister Hassan Diab has come to power in Lebanon, but it is already broadly unpopular and faces an uncertain future, despite surviving a parliamentary no-confidence vote this week. In Iraq, mass anti-U.S. protests sparked by the killing of General Suleimani have tapered off since Shia cleric Moqtada Al Sadr called on his followers to clear the streets in a show of support for the new prime minister, Mohammed Allawi. However, Allawi has little political leverage in parliament and faces opposition from anti-government protestors who believe he represents the political establishment.

The size of the protests over the past year, their stated democratic ambitions, and their initial success in toppling unpopular leaders bear striking similarity to the 2011-12 Arab Spring. In the year ahead, we will be watching how Sudan, Algeria, Lebanon, and Iraq navigate this period of political tension, and whether the unrest remains limited to these countries, or, as was the case with the Arab Spring, fuels wider instability across the region including in the Arab Gulf states.

Below are four scenarios that could unfold this year:

- Status quo (most likely): Unrest continues without a clear path to political resolution. While protests in Sudan have declined significantly, unrest is likely to continue over the near-term in the other three countries. In Algeria, the military has managed to calm protests somewhat in the short-term by proposing talks and appointing new faces to senior government posts, but this strategy of playing for time is unlikely to satisfy protestors in the long-term. In Lebanon, anti-government protests are likely to continue, especially if the Diab government falls and Parliament is unable to agree on a new government. In Iraq, Prime Minister Allawi faces an uphill battle in both forming a cabinet and satisfying the demands of anti-government protestors.

- Escalation (credible alternative): The unrest worsens in some or all of the countries, possibly resulting in longer-term instability or civil war. If dialogue breaks down between the military and protestors in Algeria, protests could spiral, and the military could resort to violence to maintain control. Lebanon and Iraq are at especially high risk for civil conflict given the scale of ongoing protests, the depth of popular dissatisfaction with political elites and the economic situation, and both countries’ history of sectarian conflict and civil war.

- Transition (outlier): The countries put the worst of the unrest behind them either through democratic transition or return to control by political elites. Sudan has the best chance of achieving stability and a longer-term transition to democracy if the civilian-military power sharing agreement holds. In Algeria, the military seems likely to cement its control in the near term, though this will depend on its ability to continue to curb protests without provoking further opposition. In Lebanon and Iraq, deeply entrenched confessionalism will make it difficult to bridge divisions among both the political elites and the opposition, and political stability—whether in the form of control by a unified political elite or transition to functioning democracy—is likely to be elusive.

- Arab Spring 2.0 (outlier): Unrest spreads to other countries, fueling regional instability and economic disruption. During the Arab Spring, protests broke out almost simultaneously in several countries and spread across the region within a just a few months of the overthrow of the government in Tunisia. This time, the unrest has not taken the shape of a regional movement, and the protest movements in Sudan, Algeria, Lebanon, and Iraq do not appear to be closely linked. However, the economic and political drivers of the Arab Spring are still present and have the potential to fuel wider regional unrest. While the protests in Iran mentioned above signal significant popular dissatisfaction with some of the same root causes as those in Iraq and Lebanon, the regime’s tight grip on power continues to make a large-scale uprising unlikely. Other oil exporters also enjoy tight political control; however, they have also cut the generous oil subsidies they have historically relied on to pacify domestic unrest.

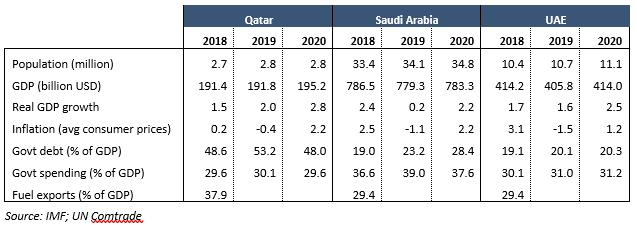

Gulf economies had a difficult year in 2019. With the exception of Bahrain and Qatar, which saw modestly improved growth, the GCC economies all slowed relative to 2018. Overall GDP growth dropped from 2.0% to 0.8%, the second-weakest aggregate growth since the global financial crisis. While the UAE economy slowed only negligibly from 1.7% to 1.6% growth, Kuwait saw its economic growth fall by half from 1.2% to 0.6%, and Saudi Arabia experienced an even steeper slowdown from 2.4% to 0.2% growth. The Omani economy ground to a halt, registering no growth in 2019 after growing 1.8% the year before. The slowdown tracked low oil prices, which cut into economic growth and government spending across the region, and a slowing global economy

3. Gulf economies poised for recovery after tough 2019

Gulf economies had a difficult year in 2019. With the exception of Bahrain and Qatar, which saw modestly improved growth, the GCC economies all slowed relative to 2018. Overall GDP growth dropped from 2.0% to 0.8%, the second-weakest aggregate growth since the global financial crisis. While the UAE economy slowed only negligibly from 1.7% to 1.6% growth, Kuwait saw its economic growth fall by half from 1.2% to 0.6%, and Saudi Arabia experienced an even steeper slowdown from 2.4% to 0.2% growth. The Omani economy ground to a halt, registering no growth in 2019 after growing 1.8% the year before. The slowdown tracked low oil prices, which cut into economic growth and government spending across the region, and a slowing global economy.

Despite all setting ambitious long-term strategies for economic diversification, the GCC countries remain highly dependent on oil. The mixed track record of Saudi Vision 2030 is emblematic of the challenges Gulf countries face as they seek to transition away from oil. The Saudi government has poured tens of billions of dollars into health, education, infrastructure, and tourism, unveiled flagship megaprojects designed to attract foreign visitors and investors, streamlined regulations to make the country more competitive, and imposed a quota-based system to encourage hiring of Saudi nationals. The Kingdom has largely succeeded in improving its investment climate, recording a 54% year-on-year increase last year in the number of new foreign investment licenses. In Q3 2019, Saudi Arabia also had its strongest non-oil sector growth since 2014. However, broader efforts to reduce dependence on oil exports for government revenue and on government hiring for employment have fallen short of targets. The Kingdom still depends on oil for more than 85% of government revenue, and although the official unemployment rate among Saudi nationals dropped from 12.9% in mid-2019 to 12.0% in Q3 2019, absolute private sector employment of Saudi nationals actually dropped.

We will continue to monitor whether Saudi Arabia and other Gulf countries press ahead with economic diversification efforts and fiscal tightening, or take advantage of stabilizing oil prices to relax fiscal and economic policy.

The IMF expects Gulf economies to recover this year on the back of expected stabilization in oil prices and global economic growth. Over the coming year, we will be watching whether the geopolitical risks that have roiled international markets in recent years—especially trade tensions with China—level off as expected. A flare-up in trade tensions, increase in uncertainty over Brexit, or re-escalation of hostilities with Iran could all increase volatility in global oil and financial markets. Regionally, we will continue to monitor whether Saudi Arabia and other Gulf countries press ahead with economic diversification efforts and fiscal tightening, or take advantage of stabilizing oil prices to relax fiscal and economic policy. Looser fiscal policy could stimulate short-term growth but at the risk of the longer-term fiscal health of GCC countries.

We see three scenarios for the year ahead:

- Improvement (most likely): Gulf economies modestly recover and make incremental progress with reforms. Barring significant external headwinds such as a steep decline in oil prices or re-escalation of trade tensions with China, we expect the Gulf economies to recover to modest growth this year. An uptick in regional economic growth would give a boost to the ongoing economic reform initiatives in many of the Gulf countries. Though reform agendas like Vision 2030 are likely to miss some of their more ambitious targets in the near term, we nevertheless expect to see incremental progress this year.

- Stagnation (credible alternative): Gulf economies do not recover as expected, putting pressure on state finances and undermining reform efforts. A significant decline in oil prices, while relatively unlikely given the commitment by OPEC and its allies to continued production cuts, would pose a direct risk to economic recovery in the Gulf countries. Lower-than-expected growth this year could place the Gulf countries under pressure to cut government spending accordingly, at the expense of investments in longer-term economic reform and diversification, or risk ballooning deficits.

- Disruption (outlier): The economic outlook regionally or in individual countries worsens, stalling reform efforts and spurring public dissatisfaction. While a downturn in Gulf economies this year currently appears unlikely, a combination of serious regional and external headwinds—such as a reescalation of regional tensions with Iran and/or a sharp drop in oil prices, coupled with external disruptions to the global economy—could lead to significant economic disruption. However, a regional downturn remains less likely than a disruption in individual Gulf countries. Oman, in particular, is in a vulnerable position after years of economic stagnation and growing deficits and the death of Sultan Qaboos in January. Failure of Qaboos’ successor, Haitham, to adequately address the country’s economic and financial challenges could result in growing public dissatisfaction with the economy and raise the risk of political unrest.

About ASG

Albright Stonebridge Group (ASG) is the premier global strategy and commercial diplomacy firm. We help clients understand and successfully navigate the intersection of public, private, and social sectors in international markets. ASG’s worldwide team has served clients in more than 120 countries.

ASG's MENA Practice has extensive experience helping clients navigate markets across the Middle East and North Africa. For questions or to arrange a follow-up conversation please contact Michael Bessey.