ASG Analysis: Strategic Opportunities in the MENA Fintech Sector

Key takeaways

-

The adoption of fintech solutions is expanding rapidly in the Middle East & North Africa (MENA), and many regional governments are actively shaping their policy and regulatory environments in response to growing demand.

-

Several countries – especially Saudi Arabia, Israel, and Bahrain – are advancing open banking regulations and other fintech-enabling legislation. Some of these regulations are set to be implemented as soon as early 2022. Companies seeking a voice in shaping these policy environments should look for ways to engage with relevant government officials.

-

The region’s digital payment sector exploded in 2020, and competition is increasing quickly. Companies operating in the digital payments space should explore ways to address specific market needs and partner with regional governments to advance national goals for becoming cashless economies.

-

Fintech companies have the option of partnering or competing with traditional MENA banks as they race to digitize their own services and satisfy consumer demands for more efficient, cutting-edge financial solutions.

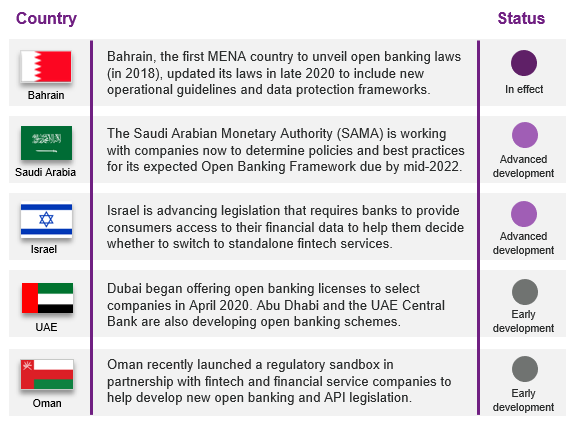

1. MENA countries introduce open banking laws and other fintech-enabling regulations

The introduction of open banking laws, which enable third-party fintech companies and application programming interfaces (APIs) to access, process, and integrate financial information across various accounts, is a game-changer for MENA. These new laws will unlock an array of opportunities for fintech companies, push banks to modernize their services, and raise expectations for digital financial services.

However, as is common across many fintech markets, both consumers and banks across the region have raised questions about open banking laws and the safest and most effective policies for sharing financial information. Since most of the region’s open banking regulations are in their nascent stages, the landscape is ripe for industry leaders to help government stakeholders develop policies that safeguard consumer interests and establish new ecosystems that define and harmonize relationships between banks, fintech providers, and regulators.

Below are status updates on the key open banking laws being developed in the region.

2. The digital money transfer, remittance, and payment sub-sector is growing rapidly

Although the region’s digital payments industry was already registering high growth before Covid-19, the sector exploded during the pandemic. The number of e-commerce users in the UAE grew by approximately 70 percent in 2020. Transactions on Bahrain’s public immediate payment service rose more than sixfold year-on-year in 2020. Together, the UAE and Saudi Arabia handled $78 billion-worth of digital transactions, equaling 7 percent of their combined GDPs. The overwhelming opinion across most surveys and reports is that the region’s shift to cashless is permanent and will accelerate over the next five years, driven in large part by an aggressive push by regional governments for a whole-scale transition to cashless economies.

Competition in the space is increasing quickly as MENA consumers become more selective of their digital payment services. For example, a recent survey of Saudi companies found that 65 percent were looking for “better, more efficient” digital payment options than those currently offered. Among the key players that make up the region’s industry are:

Long-standing industry players, which have dominated much of the region's digital payment sector until now, such as PayPal, alphabet, ACI Worldwide, and Samsung Pay.

High-growth startups and apps, which were downloaded 9.5 million times and handled around $6.9 billion worth of digital transactions in 2020 - representing a sizeable portion of the region's remittance and peer-to-peer payments.

Digital wallets and instant payment schemes offered by regional and central banks, such as the Emirates Digital Wallets Initiative to create an e-wallet across 16 leading UAE banks.

Digital payment companies should continue to develop their strategic value propositions to cater to specific market needs. Companies that can demonstrate their commitment to helping regional governments advance their national e-payment goals will also stand out. For example, Saudi Arabia aims to digitize 70 percent of its payments by 2025 and has welcomed conversations with industry leaders on how to advance this objective. Egypt also implemented its major E-Payments Act in September 2021, which requires most public and private entities to digitize large segments of their employee salary payments, supplies dues, and tax payments. Egypt’s Central Bank began granting its first licenses to digital payment companies this summer.

3. Financial institutions can decide whether to partner or compete with regional banks as they race to digitize

Traditional banks in MENA are under pressure from consumers and governments to significantly expand their digital service offerings. Many regional banks still do not process credit card payments in real-time, provide personalized investment recommendations based on big data analysis of financial records, offer digital crowdfunding options, or accept online loan applications. Regional banks will rely heavily on new partnerships with fintech companies to fill these gaps and integrate fintech into their overall strategies. A recent McKinsey survey found that 73 percent of MENA respondents thought regional banks should acquire fintech firms to “stay relevant.”

Companies that partner with regional banks benefit from high investments from their partner banks and governments, possible regulatory or tax breaks, and streamlined licensing procedures. Some recent examples in the region include: Germany’s Mambu, which offers software to help banks build digital platforms, opened an office in Abu Dhabi in November 2020 in partnership with Banque Saudi Fransi; U.S.-based Stripe partnered in April 2021 with Network International, a subsidiary of Emirates Bank, to introduce a new UAE payment solution; and Dubai’s NOW Money, a neobank startup, partnered with the Commercial Bank of Dubai in October 2020 to expand the bank’s digital services.

For some companies, the better strategic option is to market their services as standalone or to partner with multinational financial service companies seeking to expand their regional footprints. This latter option has recently driven several major industry players, such as Visa, Mastercard, and Western Union, to enter long-term partnerships with promising MENA startups and access an extended consumer base estimated to be close to 3 billion people.

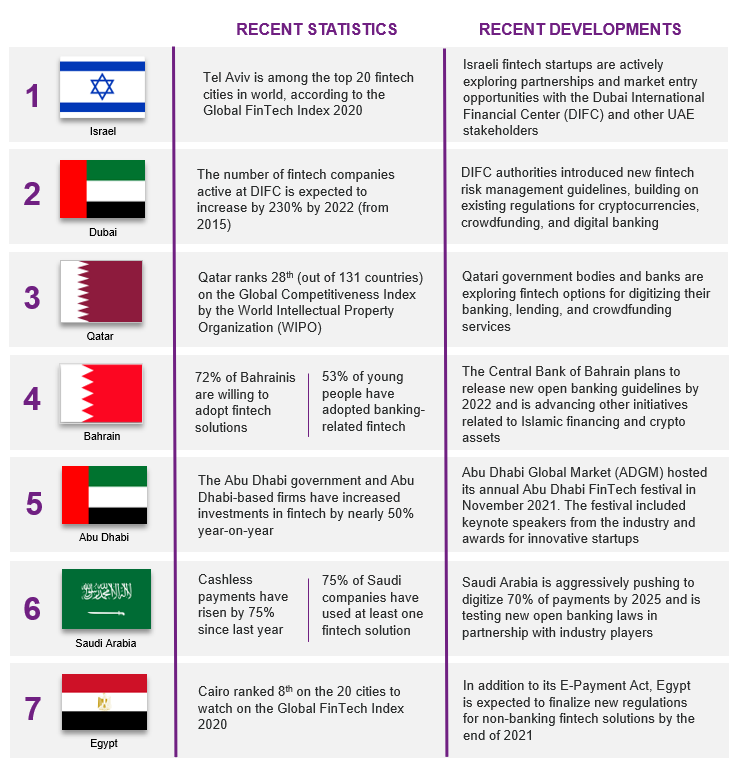

Key markets

About ASG

Albright Stonebridge Group (ASG), part of Dentons Global Advisors, is the premier global strategy and commercial diplomacy firm. We help clients understand and successfully navigate the intersection of public, private, and social sectors in international markets. ASG’s worldwide team has served clients in more than 120 countries.

ASG's Middle East & North Africa practice has extensive experience helping clients navigate markets across the region. For questions or to arrange a follow-up conversation please contact Louise Rosenberg.